SKYROCKET TO SUCCESS WITH A MENTOR

FOR NEWBIE INVESTORS:

CONFUSION → CLARITY

→ CASH FLOW

We teach newer cash strapped investors :

Seeking quicker cash flow and financial security

How to earn big profits, by adding value and fixin' up small investment properties.

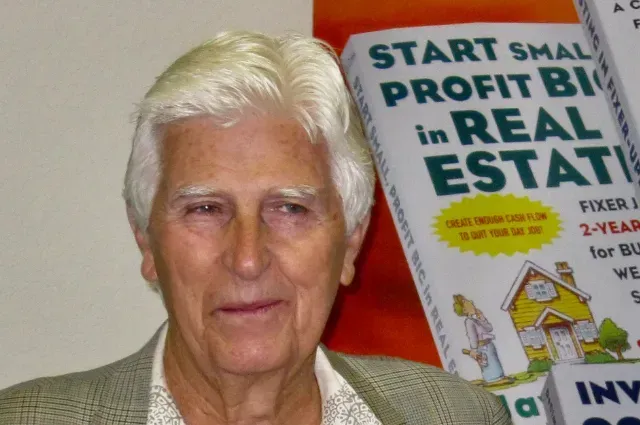

Fixer Jay Has Been Featured in Many Publications

Life Does Not Get Better BY Chance,

It Gets Better By Change.

Jim Rohn

Jay Receives Prestigious Jim Rohn Award Inspired by Jim Rohn

Nixon Library, California - September 2018

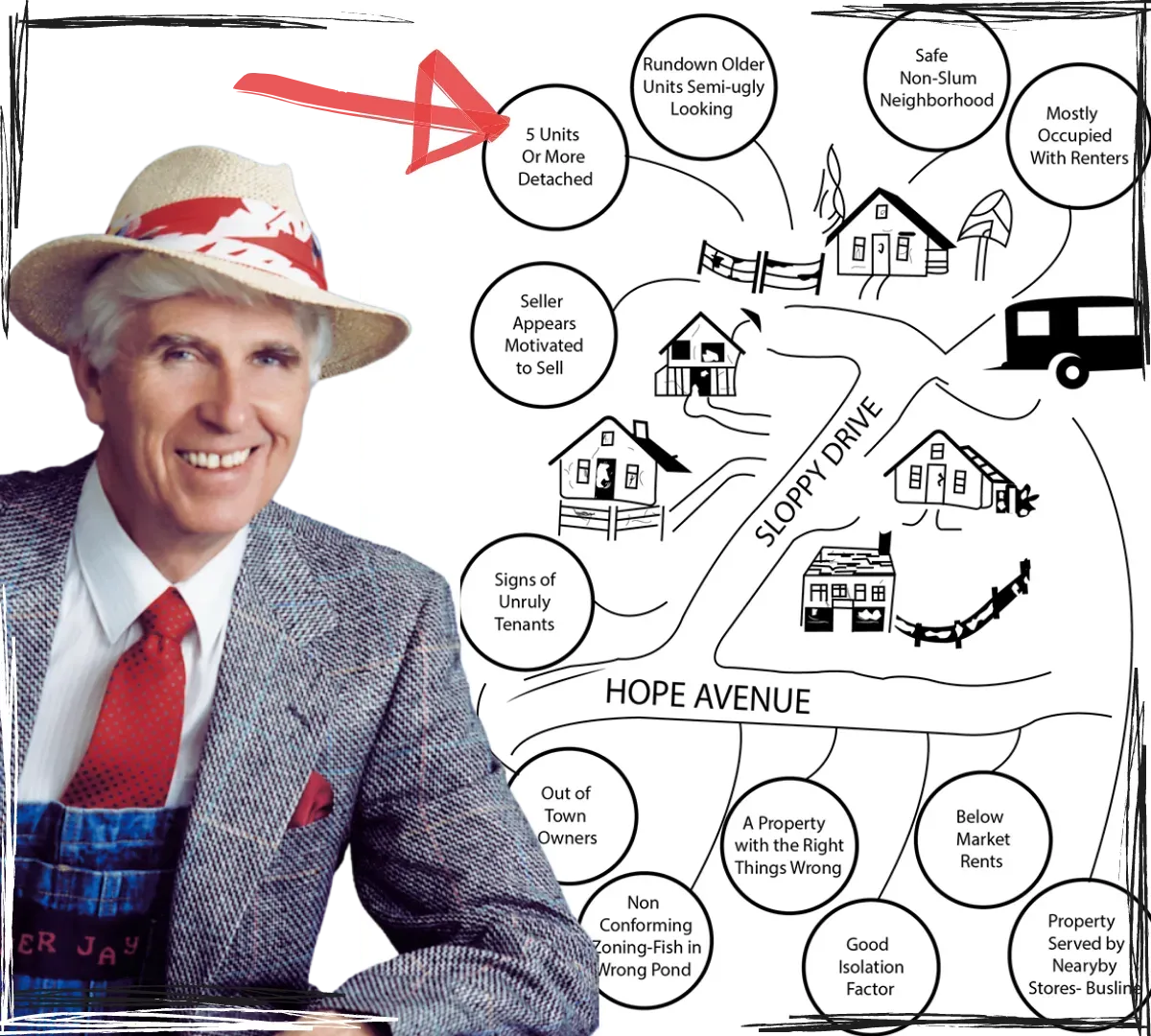

We Help Newbie Investors Focus On The Right Kind Of Cash Flow Properties - STOP Wasting Time!

Learn to buy groups of houses

(not just 1 at a time)

Quicker equity, more cash flow

7 Published Books Sold

Successful Students

We Are Experts In Cash Flow Real Estate Deals

Without Starting With A Boatload Of Cash!

Finding the Right Vehicle

In my case I needed to quickly develop monthly cash flow without paying a ton of cash for my properties (which I didn’t have). Only certain types of properties (vehicles) will provide cash flow, so that’s where I directed my energies.

Why Seller Financing Is So Profitable

I insist on having TOTAL CONTROL over my investments. This particularly applies to the financing when I purchase properties. Most older rundown fixer type houses should not require new bank financing. Always try to get sellers to finance the sale or most of it! Seller financing is flexible and cheaper.

Fixing the Right Stuff. Earn $10 For Every $1 Spent

People often ask me why I still keep fixing rundown houses when I obviously have enough money to buy more attractive and cleaner properties. My answer is: "Because that’s where all the money’s at!"

But Hey, Don't Take My Word For It!

See what other investors & industry leaders have to say about Fixer Jay...

"Your teachings really work!"

"Your writings and teachings are easy to understand and are always entertaining...

... And as your students will testify, they always work."

John Schaub

Real Estate Expert, investor, long time friend of Fixer Jay

"I see results..."

"I really want to thank you Jay...

...You have been an inspiration and have always been there for me and all the members of my Sacramento Club."

Dave Granzella

President, Northern California REIA

"This is so useful!"

"Jay, I loved learning from you over the years...

...But more importantly, I thank you for your wisdom and thank you for sharing that wisdom with all of us."

Mike Morrongiello

President, Bay Areal Wealth Builders REIA

We Help Newbie Real Estate Investors Find Cash Flow Properites

"The techniques I teach you are tried and tested. They have all worked for me or you won't find them here!

Most of all, the ideas and methods you will learn from me are not time-dated. They work anytime, anywhere and in almost every part of the country.

They are not a fad! Neither are they particularly sensitive to interest rates, the economy, employment or even the availability of bank loans."

© 2026 KJAY Publishing. All Rights Reserved.

Privacy

Terms of Service